The Second Product Syndrome

Why Growth Breaks MGAs Long Before Scale Saves Them

There is a particular moment in the life of a Managing General Agent that feels like arrival.

The first product is working. Loss ratios are within tolerance. Bordereaux are going out on time. The carrier is calm, maybe even complimentary. The underwriting team is no longer fighting fires daily. Finance has stopped asking existential questions about earned premium logic. For the first time, the organization feels stable.

That is usually when the second product is proposed.

It rarely arrives as hubris. More often, it arrives as confidence. We know how to do this now. The playbook is written.

The carrier relationship is stable, often with multi-year renewals in place. Distribution partners aren’t just performing; they’re asking for more. Unit economics suggest leverage: the same ops team, the same systems, the same compliance infrastructure, now supporting more premium. Regulatory and licensing groundwork is already laid for adjacent lines.

The business case is real. The opportunity is genuine. And the team has earned the right to expand. They’ve proven they can execute.

This is where many MGAs begin to fail: quietly, structurally, and often invisibly at first.

Not because the second product is bad.

Not because the underwriting team is careless.

But because growth is mistaken for leverage when, in reality, it introduces weight.

This essay is about The Second Product Syndrome: the pattern through which otherwise disciplined MGAs degrade their data integrity, fracture their reporting, dilute underwriting discipline, and lose strategic clarity. Not all at once, but gradually enough that recovery becomes unlikely.

Growth does not kill MGAs.

Unmanaged complexity does.

Why the Second Product Feels Like a Natural Next Step

The decision to add a second product line often looks strategically correct.

The first product worked. Capacity is stable. Distribution is hungry. The board wants growth. The math says yes.

Sometime after launch often sooner than expected something shifts.

Not dramatically. Not visibly. But the operational texture changes. Reports take longer to close. Finance asks more questions. Carrier calls feel slightly more tense. The underwriting team seems busier but less aligned. The COO starts spending more time in reconciliation meetings and less time on strategic work.

No one made a bad decision. No one dropped the ball. The MGA that felt tight at $40M can feel loose at $55M numbers will vary, but the sensation is familiar even though headcount grew and systems didn’t change.

This is the Second Product Syndrome. And it’s not about the product itself. It’s about what the second product reveals about the infrastructure that was already quietly straining.

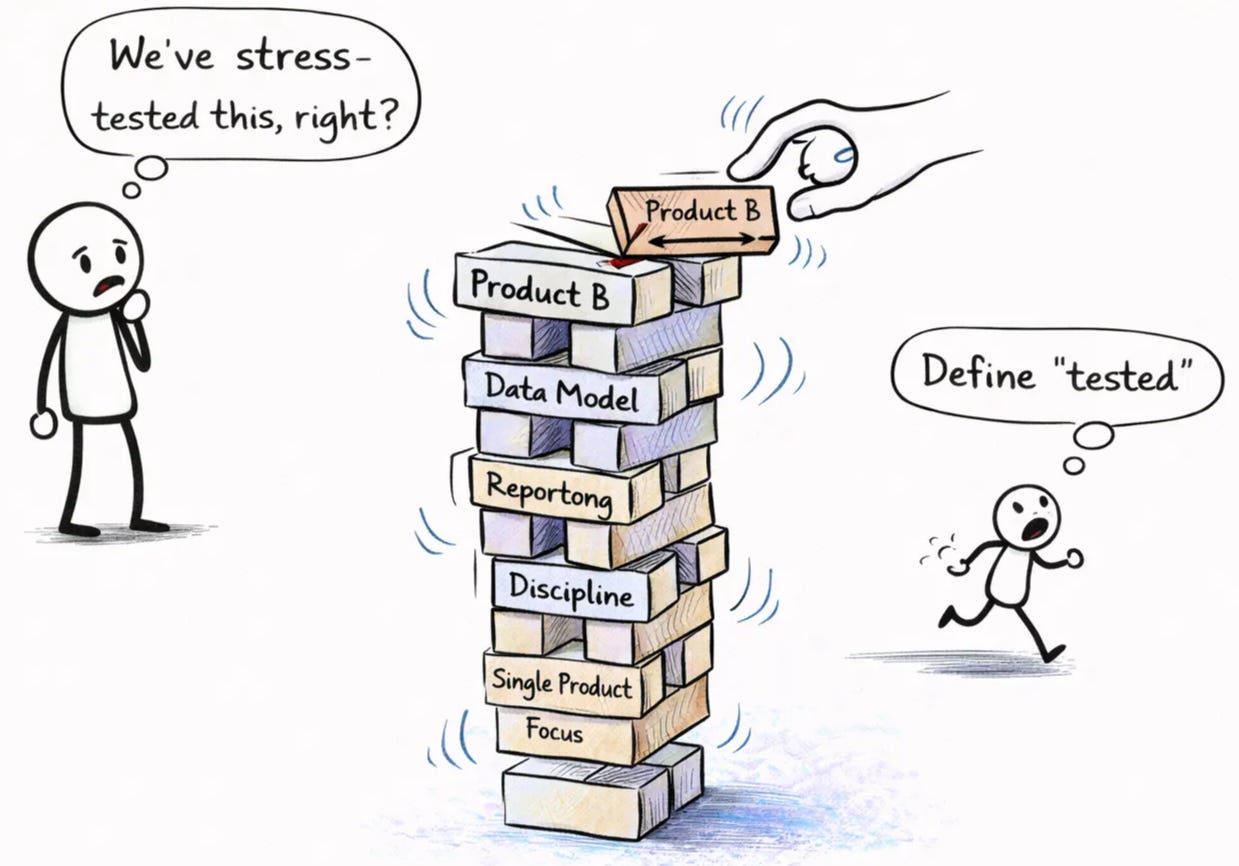

In my experience, the failure isn’t the product. It’s the complexity it reveals. They struggle because the second product exposed assumptions about data, reporting, and underwriting discipline that were never stress-tested at scale. The infrastructure that looked solid at one product was actually optimized for one product. And optimization, it turns out, is a form of brittleness.

Before we examine what breaks, it’s worth acknowledging why the decision makes sense in the first place.

The problem isn’t the strategy. The problem is the operational assumption underneath it: that the existing infrastructure will absorb the new product without fundamental strain. That assumption is where the trouble starts, and it’s almost never examined until the strain is already visible. By then, the second product is live, premium is flowing, and unwinding means admitting that the expansion was premature. No one wants to have that conversation.

What Actually Changes When You Add a Second Product

The most dangerous misconception in MGA expansion is treating a second product as if it were a SKU, an incremental addition to an existing machine.

In insurance, a product is not a SKU. It is an operating model.

A new product introduces new rating logic, new exposure definitions, new underwriting judgment boundaries, new exception handling, and often a new carrier interpretation of the same words everyone thinks they already agree on. Even when two products appear adjacent (say, GL and excess, or homeowners and dwelling fire) the internal mechanics are rarely aligned.

The first product benefits from singular focus. Every decision made early, from how policies are versioned to how endorsements are represented to how cancellations are treated, becomes a shared assumption. Over time, those assumptions harden into muscle memory.

The second product disrupts that coherence.

Suddenly, installment logic differs. Exposure units don’t roll up cleanly. Attachment points change how premium should be interpreted. Bordereau requirements diverge. Cut-off dates no longer align. The same carrier may ask for different reporting cadences for different products, even when the data originates from the same policy administration system.

This is where complexity becomes non-linear.

One product introduces variance.

Two products introduce interaction effects.

Every downstream system (reporting, finance, analytics, audit prep) now requires conditional logic. Processes that once worked universally now require forks. Workflows that were once deterministic now need human judgment layered on top. What felt like reuse becomes customization. What felt like leverage becomes drag.

You did not add a product.

You multiplied your operating model.

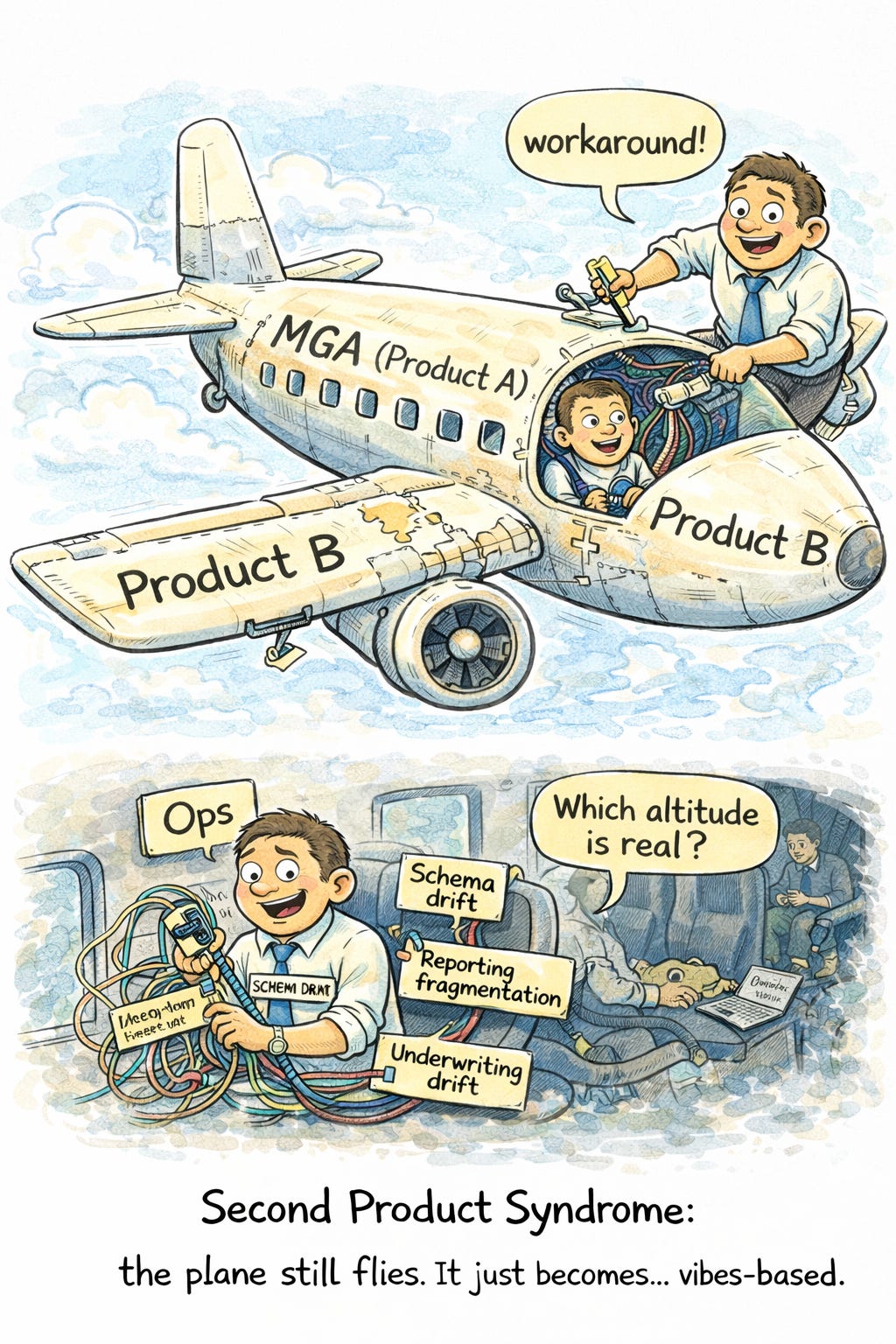

What Actually Happens Operationally

The second product doesn’t break anything immediately. It bends things.

The bending happens in three places simultaneously, each one feeding the others:

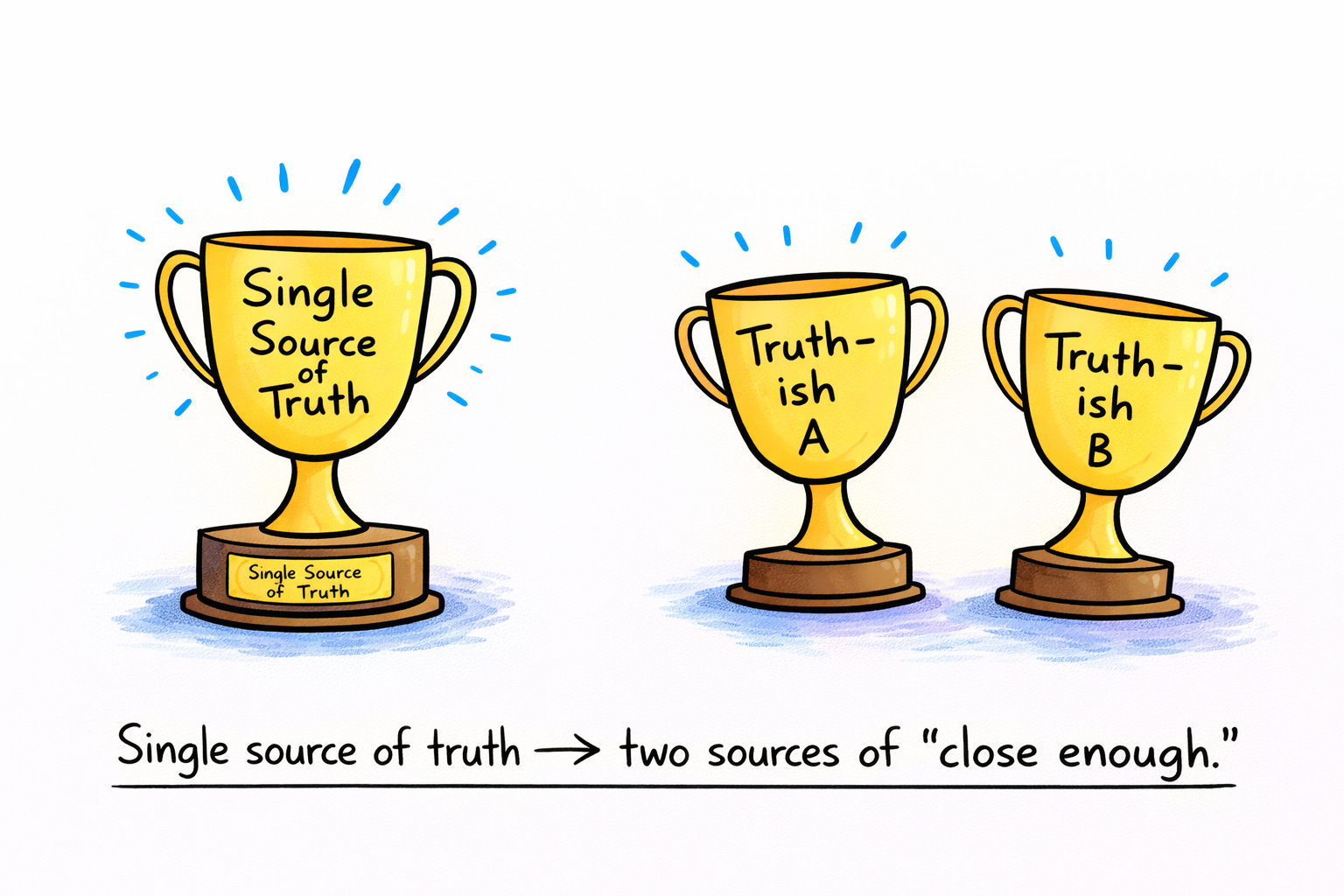

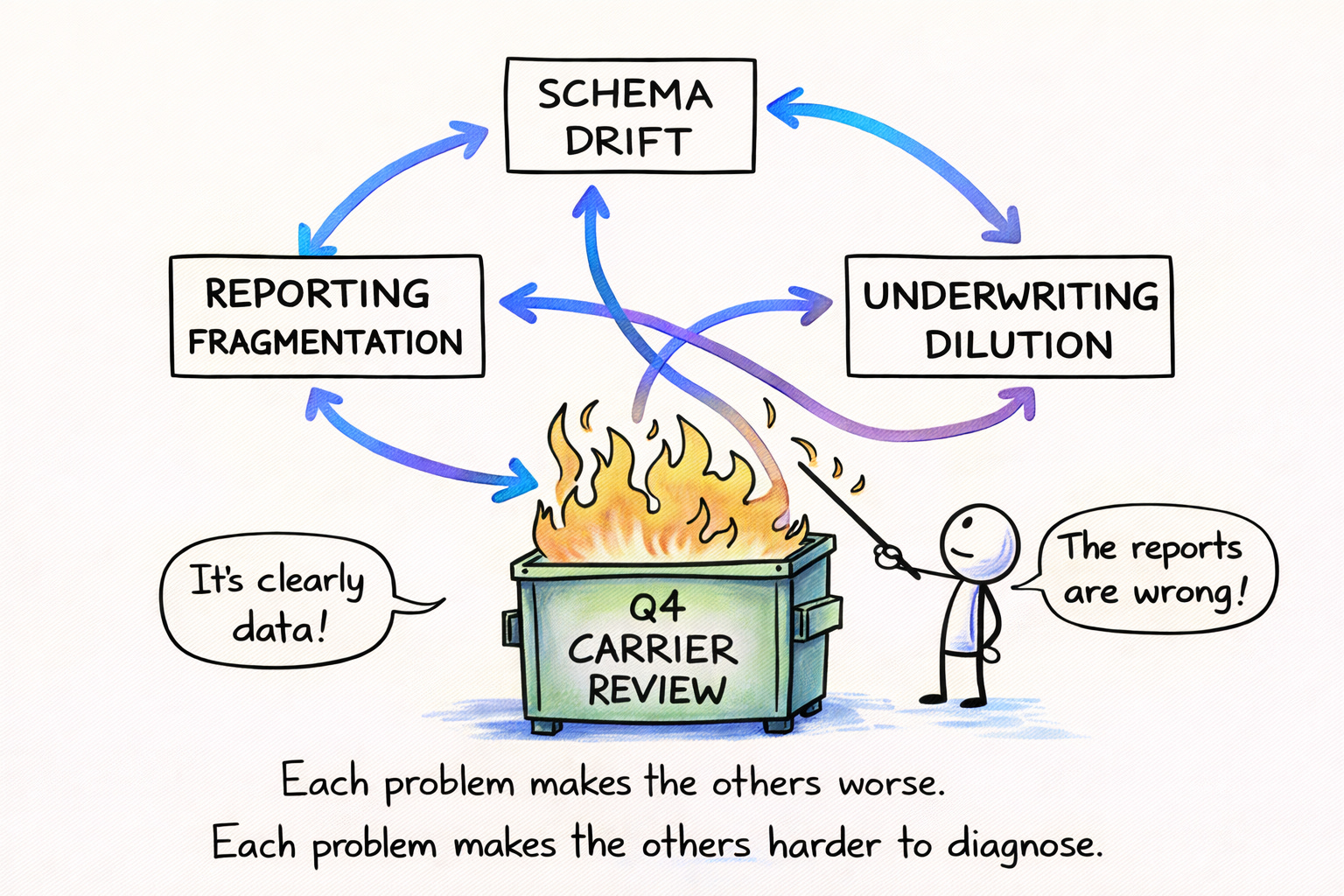

Schema drift. The data model that worked for Product A doesn’t cleanly accommodate Product B. Fields get repurposed. New fields get added inconsistently. The “single source of truth” quietly becomes two sources that don’t quite match. No one notices because both sources are technically correct; both can look internally consistent, until you try to compare them.

Reporting fragmentation. Carrier A wants bordereaux formatted one way. Carrier B (or the same carrier for a different line) wants it another way. Finance starts maintaining parallel workbooks. The monthly close stretches from a handful of days to a week, then longer.

Underwriting discipline dilution. The senior underwriter who owned Product A now oversees both. Junior underwriters get more autonomy. Guidelines that were tight get interpreted loosely. No one notices until the quarterly review surfaces anomalies, and by then, the anomalies have been compounding for months.

These three failure modes don’t stay separate. Schema drift makes reporting harder. Reporting fragmentation obscures underwriting drift. By the time anyone sees the full picture, the problems have been compounding for two or three quarters. The fix isn’t obvious because the cause isn’t obvious. It looks like a reporting problem. Or a data problem. Or a people problem. It’s actually a systems problem wearing three different masks.

Schema Drift: The First Silent Failure

The earliest structural failure caused by a second product is rarely operational. It is semantic.

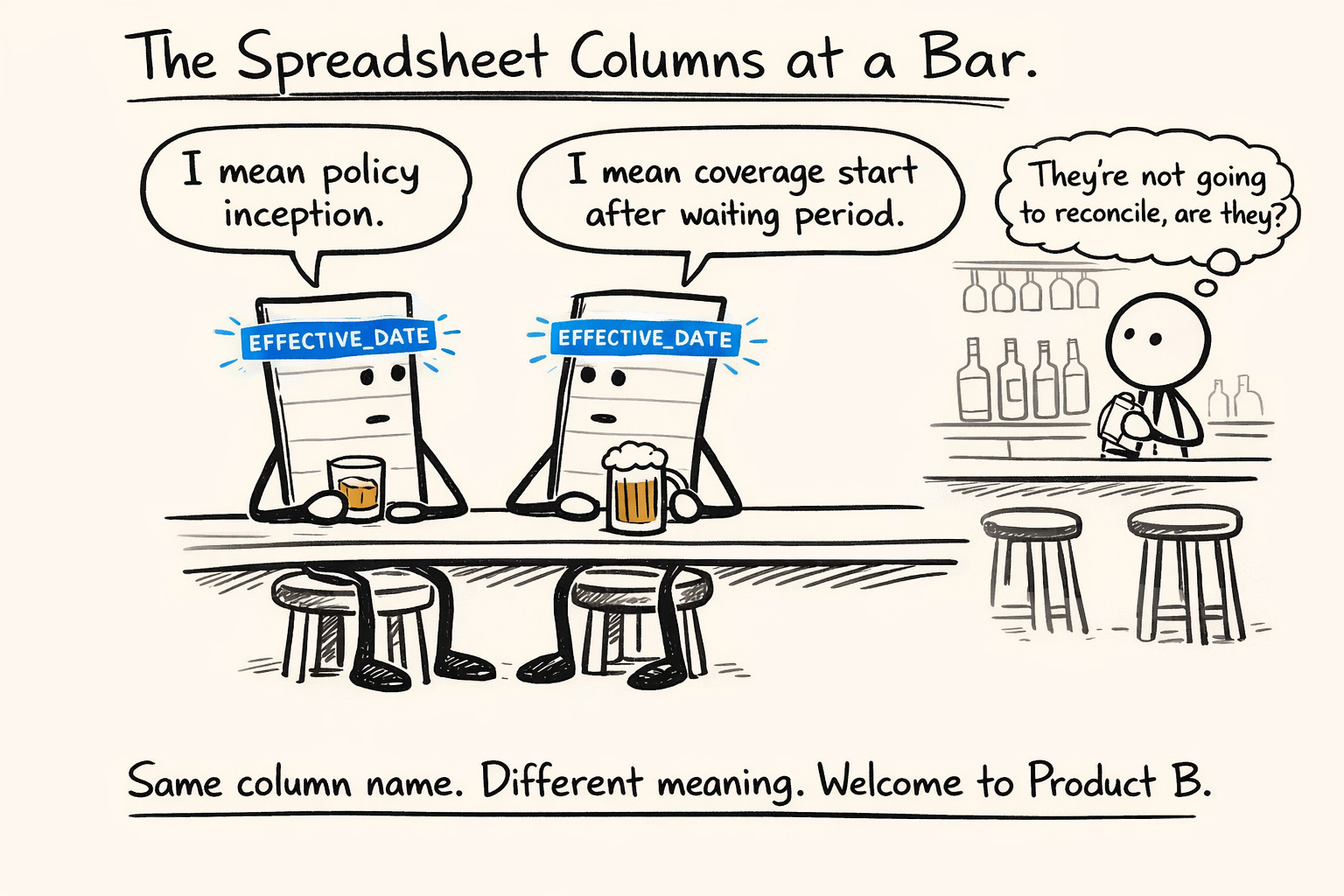

Schema drift is not a technical error. It is a meaning problem.

It begins innocently. A field that once meant one thing now means two. A column that was sufficient for Product One is reused for Product Two, even though the actuarial intent differs slightly. A policy “effective date” carries different implications depending on the product lifecycle. An exposure field that once represented a clear unit now requires interpretation.

The data still loads. Reports still run. Numbers still reconcile locally.

But the integrity is gone.

Schema drift is dangerous precisely because it does not announce itself. Dashboards remain populated. Trend lines still slope in believable directions. Stakeholders continue to feel informed, until they aren’t.

Over time, analytics become untrustworthy. Loss ratio by cohort loses precision. Comparisons between products are technically possible but conceptually flawed. Underwriting feedback loops weaken because claims signals are filtered through inconsistent definitions.

Eventually, the organization reaches a point where it can no longer answer foundational questions with confidence. Not because the answers are bad, but because no one is certain they are true.

Schema drift does not cause immediate failure.

It erodes the ability to know whether you are winning.

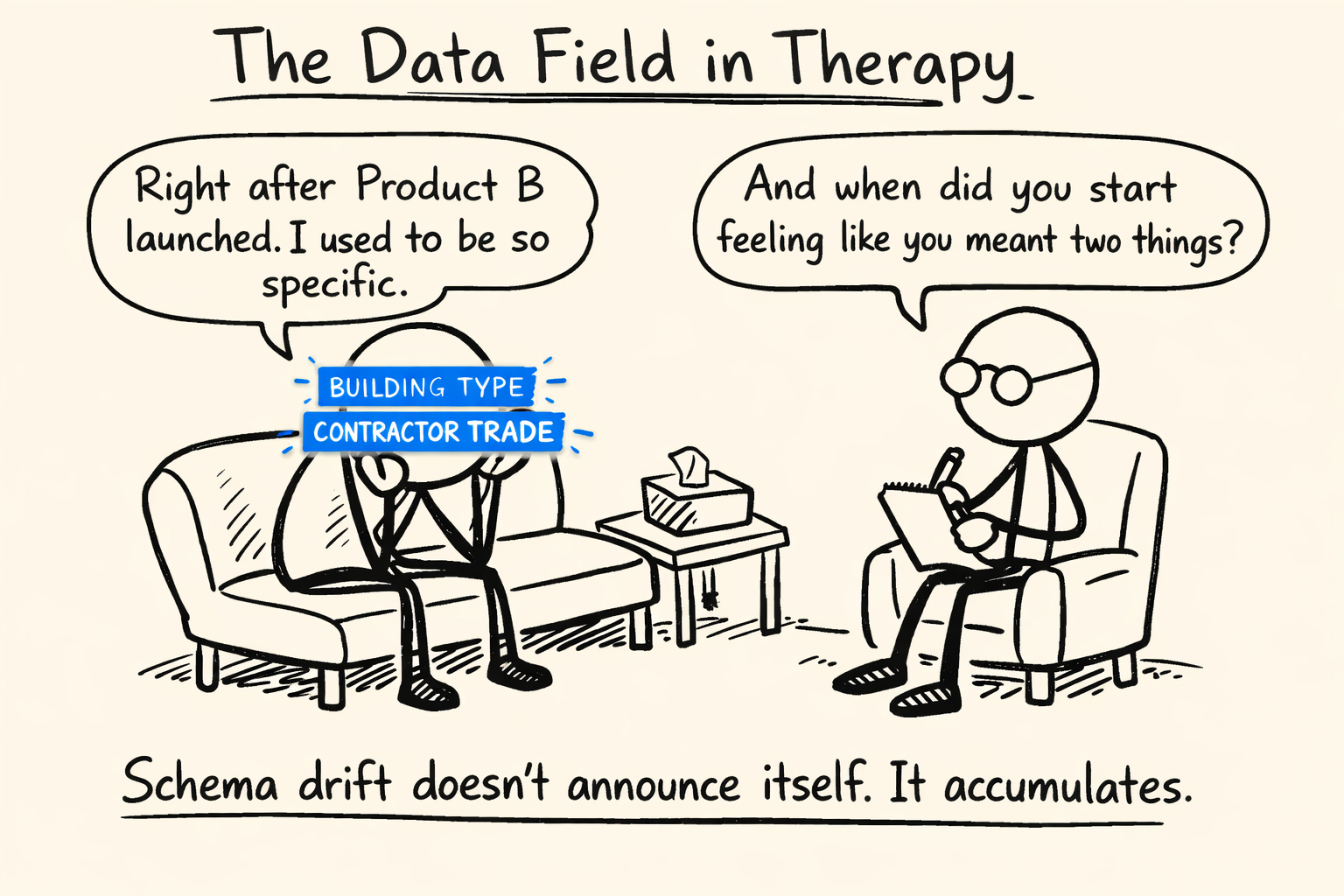

Every MGA’s data model carries assumptions from its origin story. The schema was built for Product A, its risk characteristics, its exposure structure, its carrier requirements. The schema worked because it was designed for a specific context. That specificity was a feature, not a bug.

Product B arrives with different needs. Maybe it has a liability limit structure that Product A didn’t require. Maybe it needs additional insured logic that doesn’t fit the existing fields. Maybe the location hierarchy works differently, or the classification system uses a different taxonomy. Maybe the endorsement patterns are more complex, or the premium calculation has more variables.

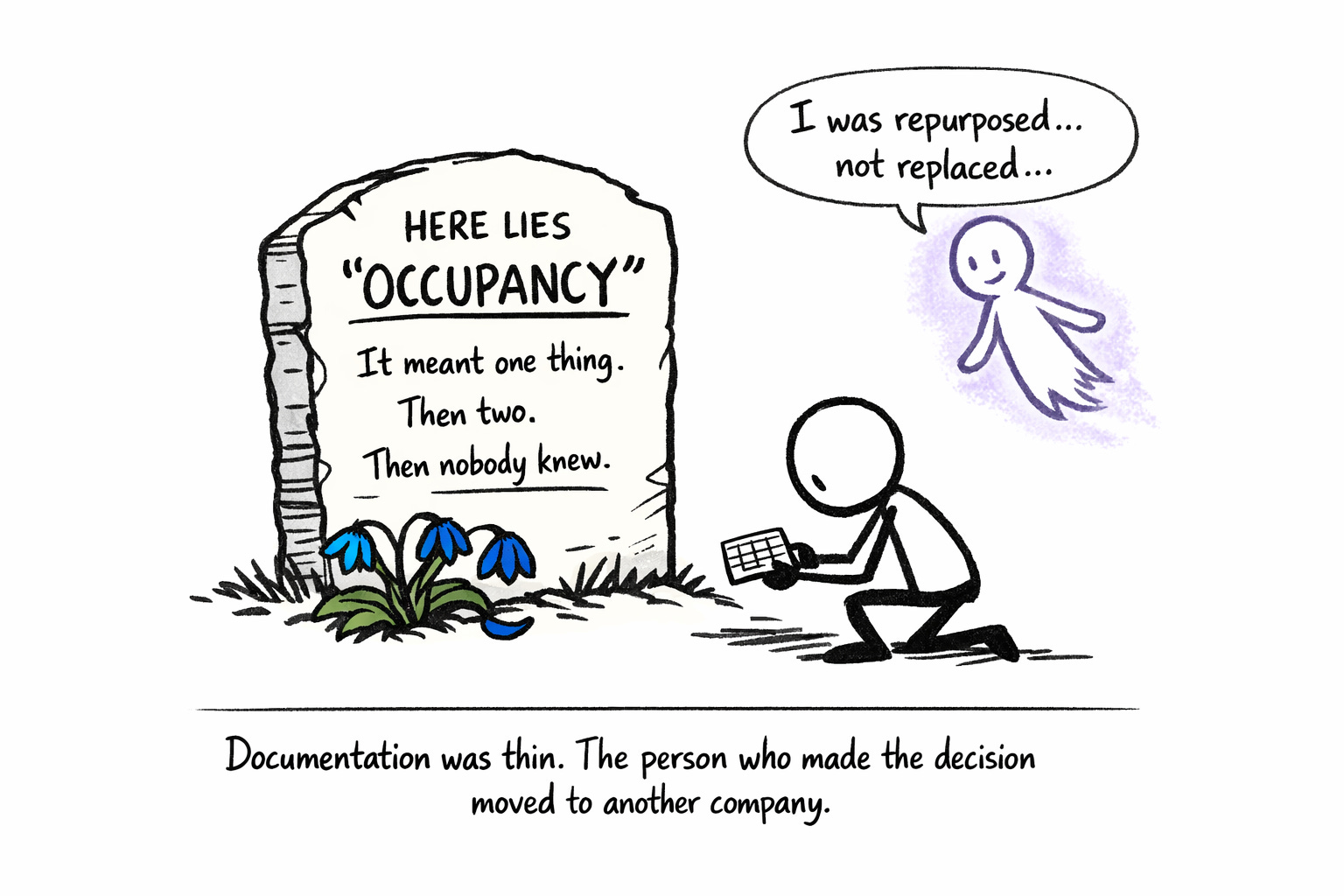

Faced with these differences, teams make a reasonable choice: rather than redesign the schema (which would mean touching every report, every integration, every downstream process) they adapt. An existing field gets repurposed. A new field gets added “just for Product B.” Documentation is thin because the person making the decision is trying to ship, not architect. They’re solving today’s problem, not anticipating next year’s audit.

Six months later, the person who made that decision may not be the person maintaining the system. The repurposed field now means different things depending on which product you’re looking at. Downstream reports pull from fields that have become semantically ambiguous. Aggregations (total insured value, premium by class, exposure counts) become unreliable without manual intervention.

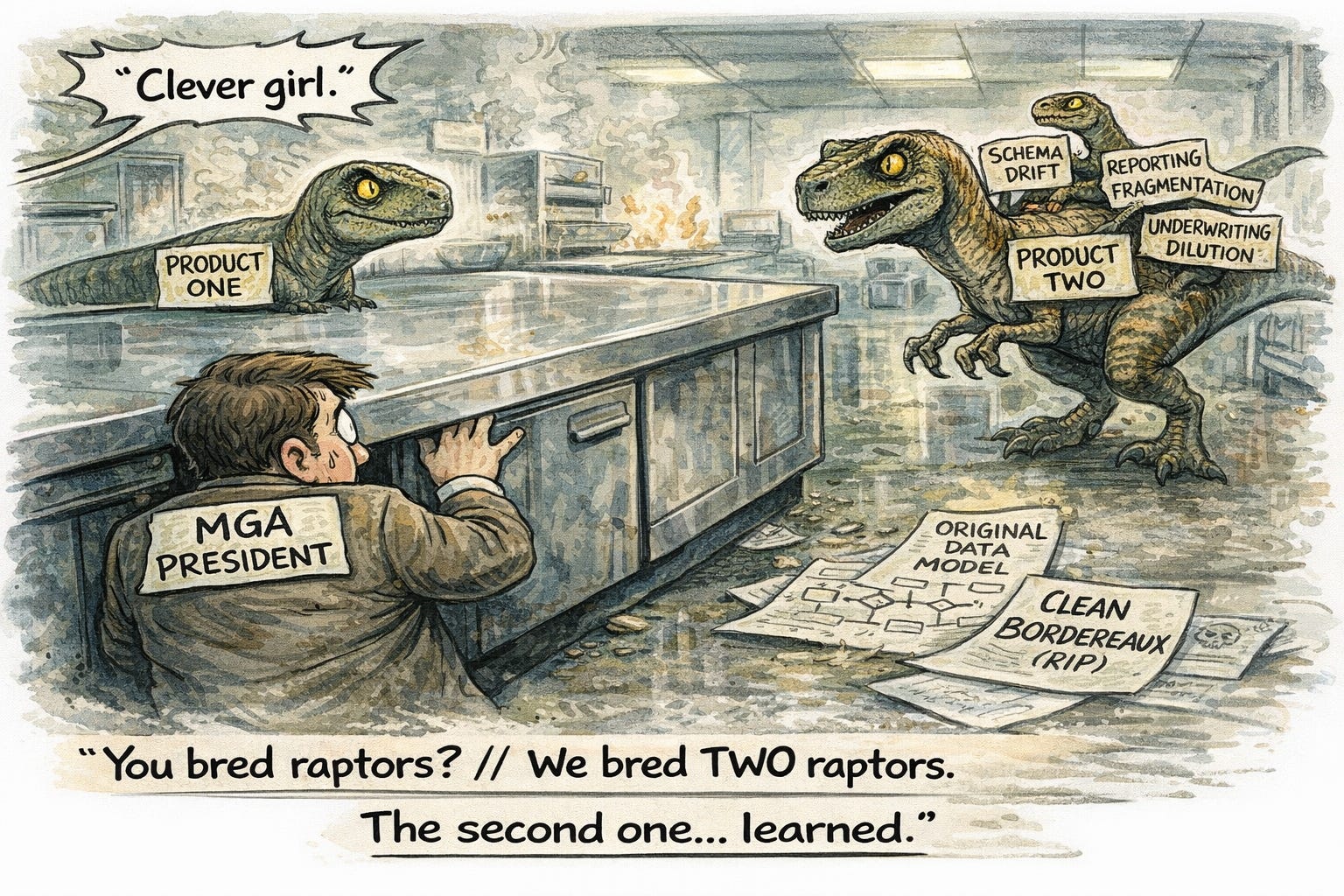

The financial consequences accumulate quietly. Audit prep time doubles because reconciliations require explanation. Bordereaux corrections become routine rather than exceptional. Carrier questions surface discrepancies that take hours to untangle, not because anyone did anything wrong, but because the data model no longer reflects a single coherent reality.

Schema drift doesn’t announce itself. It accumulates in the gaps between what the data says and what the data means. By the time it’s visible, it’s expensive.

Reporting Fragmentation: The Monthly Close Stretches

With one product, MGAs often achieve something rare in insurance: a shared version of the truth.

Finance, underwriting, and carrier partners may not agree on everything, but they agree on the core numbers. Bordereaux flow on a predictable cadence. Reconciliation logic is understood. Discrepancies are explainable.

Add a second product, and that coherence fractures.

Different products often require different earned premium methodologies. Different carriers impose different reporting standards. Cut-off dates diverge. Supplemental bordereaux appear. Finance begins to maintain product-specific adjustments. Underwriting starts running parallel reports “just to sanity check.”

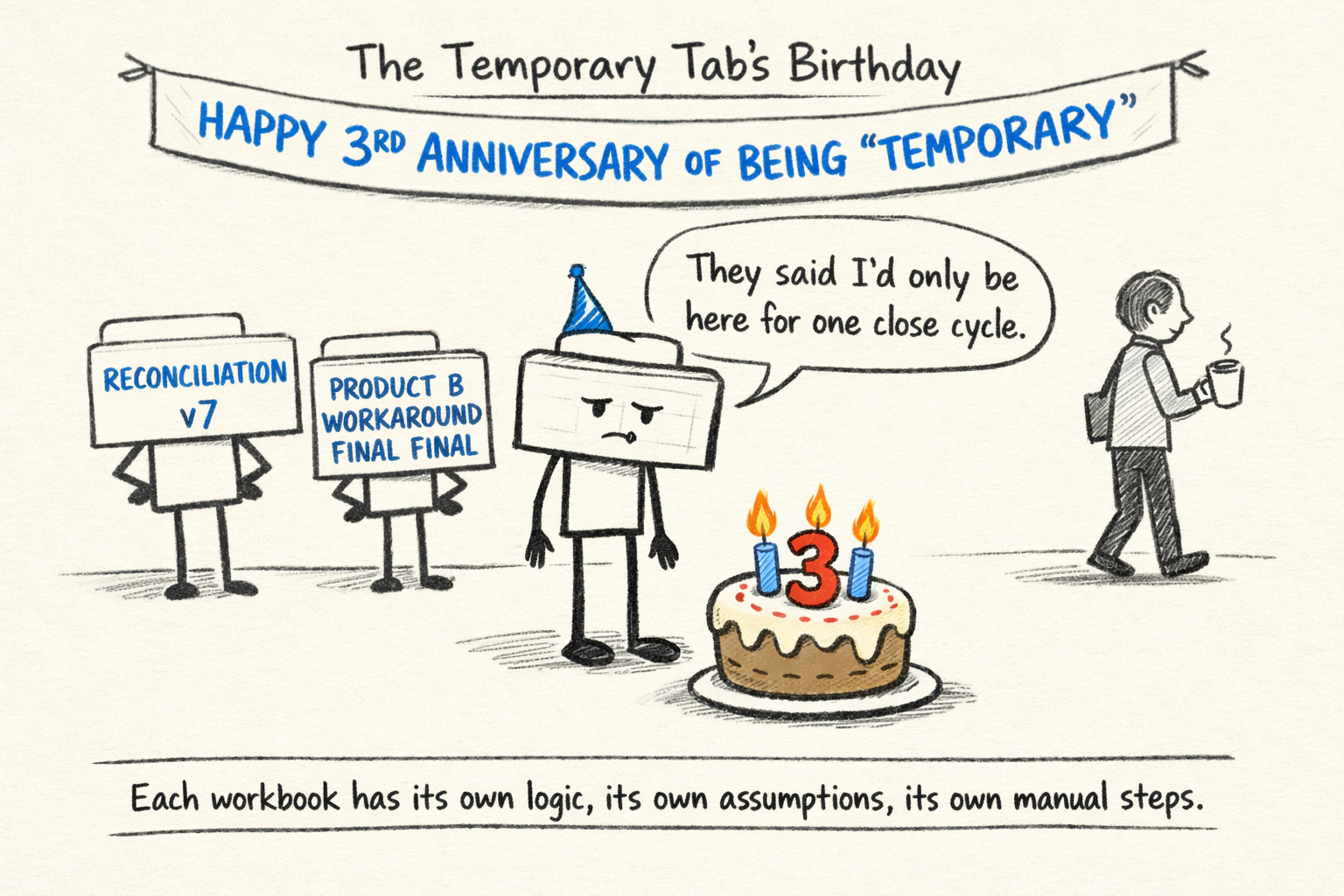

This is the spreadsheet phase.

Temporary tabs multiply. Product-specific workarounds become permanent. Institutional knowledge migrates from systems into people.

The second product typically means a different reporting relationship. Maybe it’s a different carrier entirely. Maybe it’s the same carrier but a different treaty, with different bordereaux requirements. Maybe it’s the same everything, but the line of business demands different data elements.

Whatever the reason, the reporting requirements diverge. Different templates. Different cadences. Different field mappings. Different validation rules. Different contact people asking different questions on different schedules.

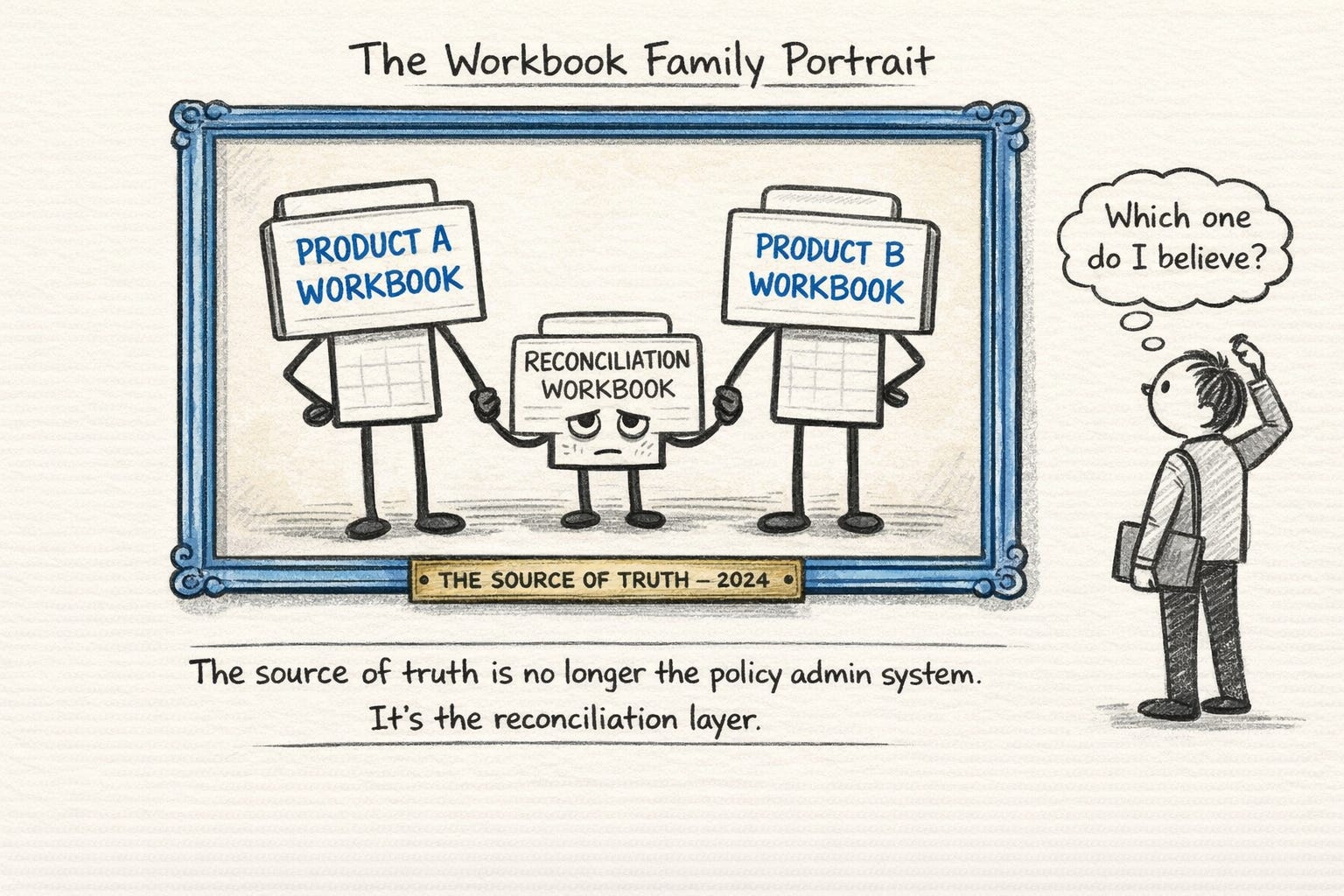

Finance responds the way finance teams always respond: they build a second workbook. Then they build a reconciliation workbook to tie the two together. Then they build a summary workbook that pulls from both reconciliation workbooks to produce management reporting. Each workbook has its own logic, its own assumptions, its own manual steps.

The “source of truth” is no longer the policy admin system. It’s the reconciliation layer: a series of manual processes that transform system data into reportable data. The monthly close, which used to be a straightforward export-validate-submit process, becomes an export-transform-validate-reconcile-re-key-re-validate-submit process. Each step introduces latency. Each step introduces error potential.

Errors get caught late. Often they’re caught by the carrier, not internally, which is worse. A carrier asking clarifying questions feels different from an internal quality check. It feels like scrutiny. It feels like the beginning of trust erosion. And trust, once eroded, is expensive to rebuild.

The human cost is real and measurable. The finance lead spends the first week of every month in triage mode, chasing down discrepancies and validating cross-product totals. Questions from underwriting (”why does this policy show X in the system but Y in the report?”) get deferred because there’s no time to investigate during close. The team is visibly busy but not productively busy. They’re maintaining a system of workarounds, not operating a system that works.

Here’s a simple diagnostic: if your close time is lengthening quarter over quarter—and cross-product totals require multiple people to validate—you’re already in fragmentation. Most MGAs don’t notice until the third or fourth product, when the fragmentation has become load-bearing and can’t be unwound without significant investment.

Underwriting Discipline Dilution: The Quiet Creep

Underwriting discipline is fragile in ways that aren’t obvious until it breaks.

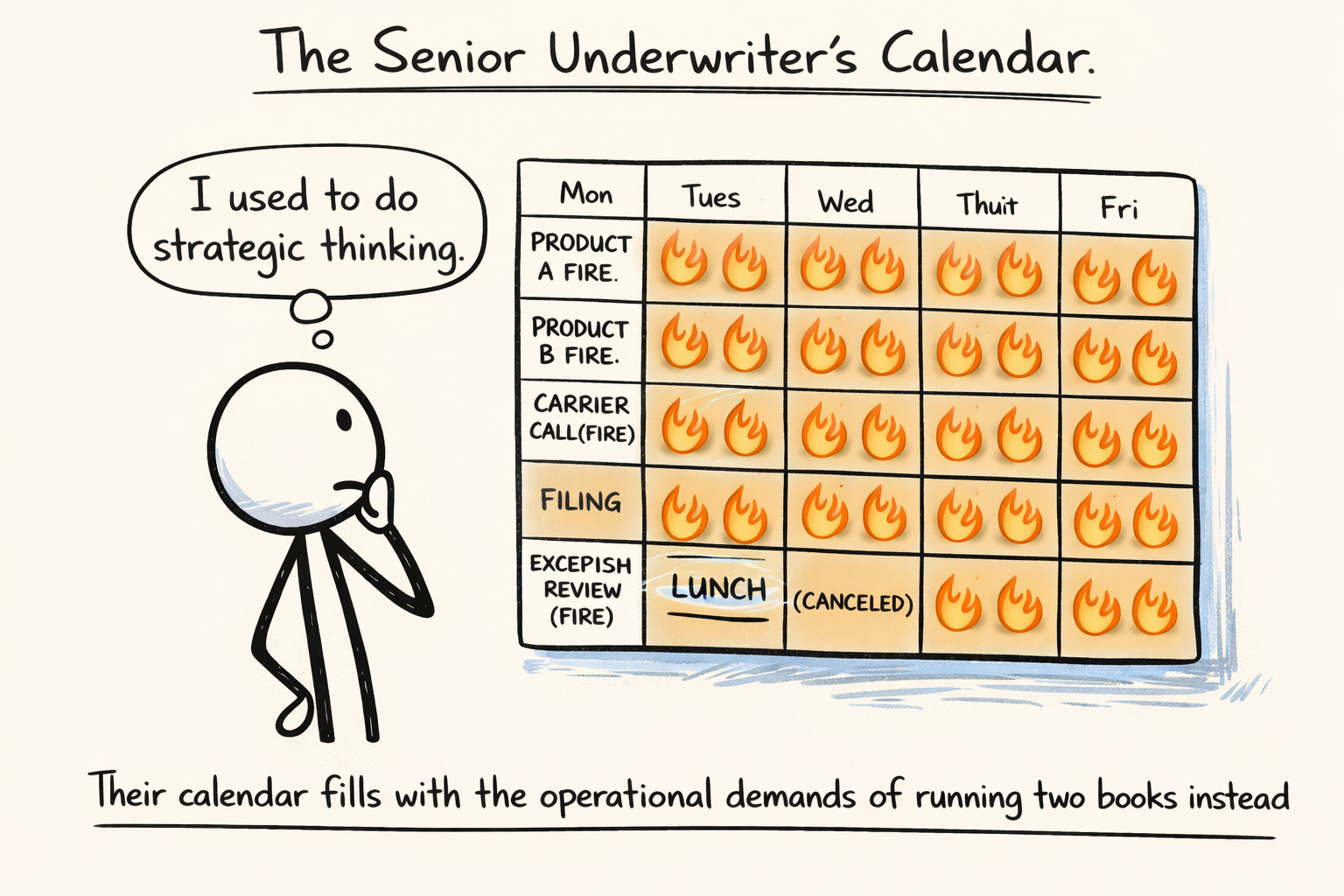

When the second product launches, the senior underwriter who owned Product A now oversees both. Their attention splits. They’re in more meetings, reviewing more submissions, answering more questions from more people about more things. Their calendar fills with the operational demands of running two books instead of one. The strategic thinking that characterized the first product’s growth phase gets crowded out by tactical firefighting.

Meanwhile, junior underwriters get more autonomy. They handle more submissions with less oversight. They make more decisions independently. This is often framed as professional development, and it is, but it’s also a reduction in the feedback loops that maintained discipline. The junior underwriter who used to get real-time coaching now gets batch feedback, if they get feedback at all.

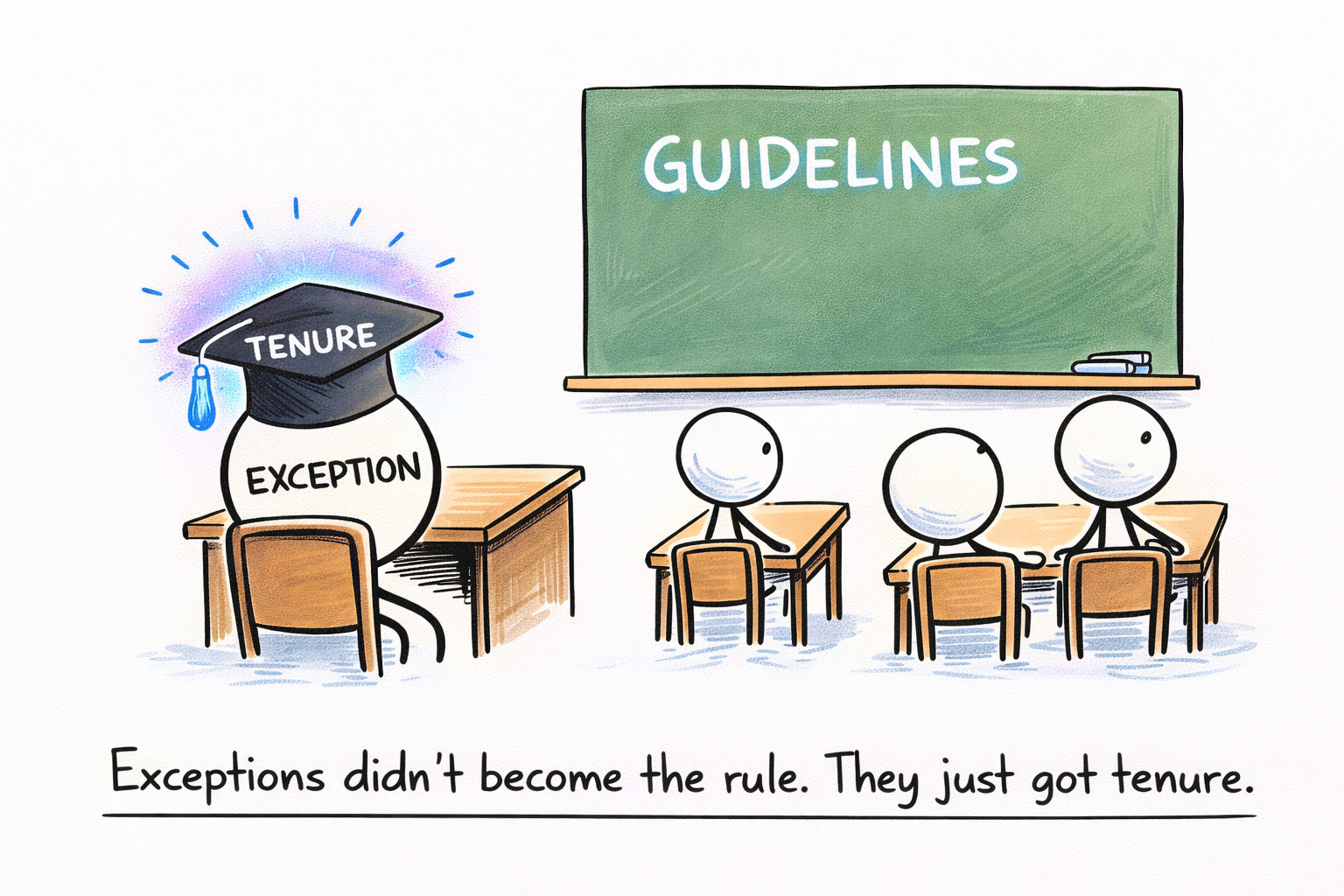

Guidelines exist, but guidelines require interpretation. Referral thresholds that made sense for Product A don’t map cleanly to Product B. Edge cases multiply. Exceptions that would have been escalated now get handled directly, because escalation means adding to the senior underwriter’s already-overwhelming queue. The path of least resistance becomes the default path.

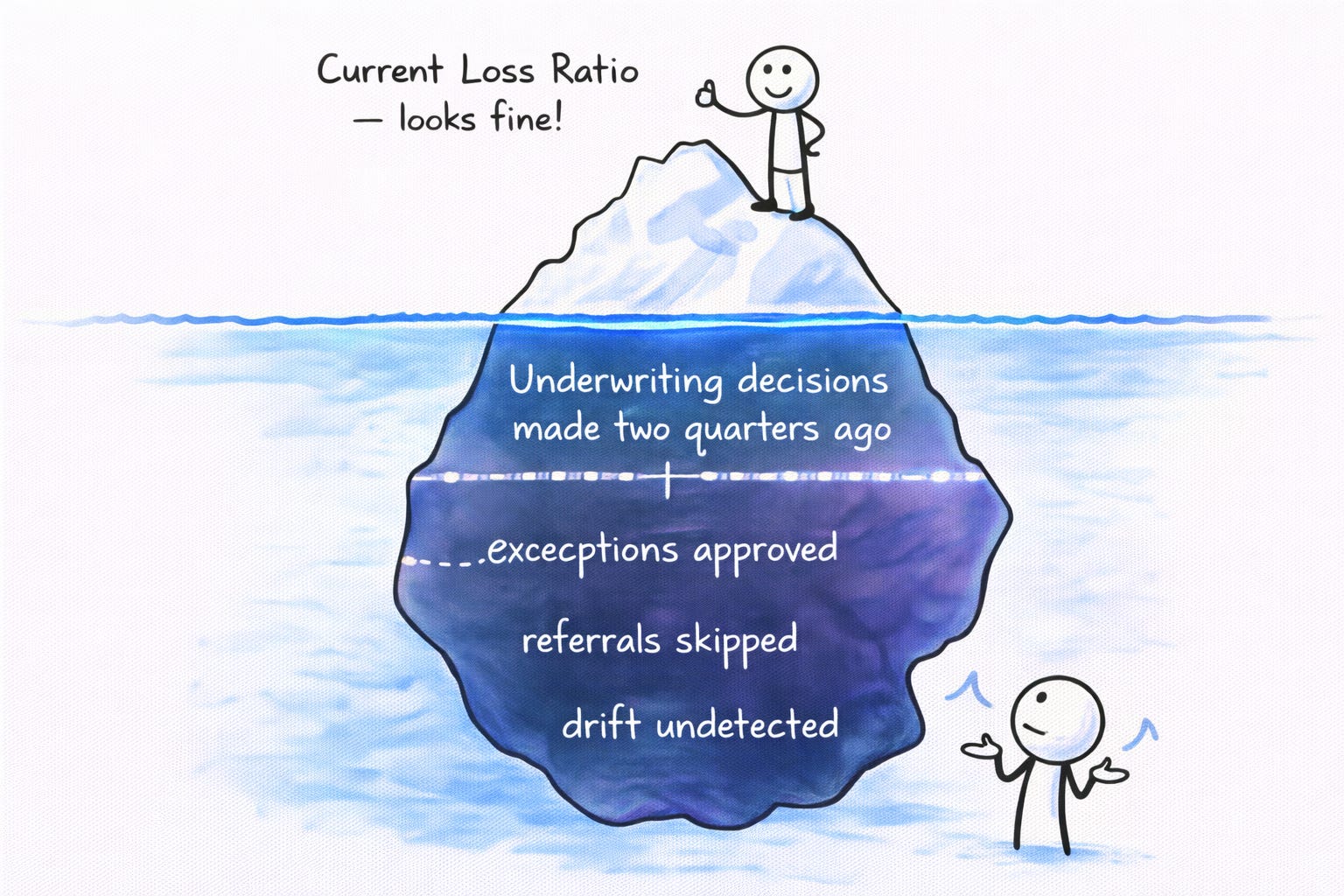

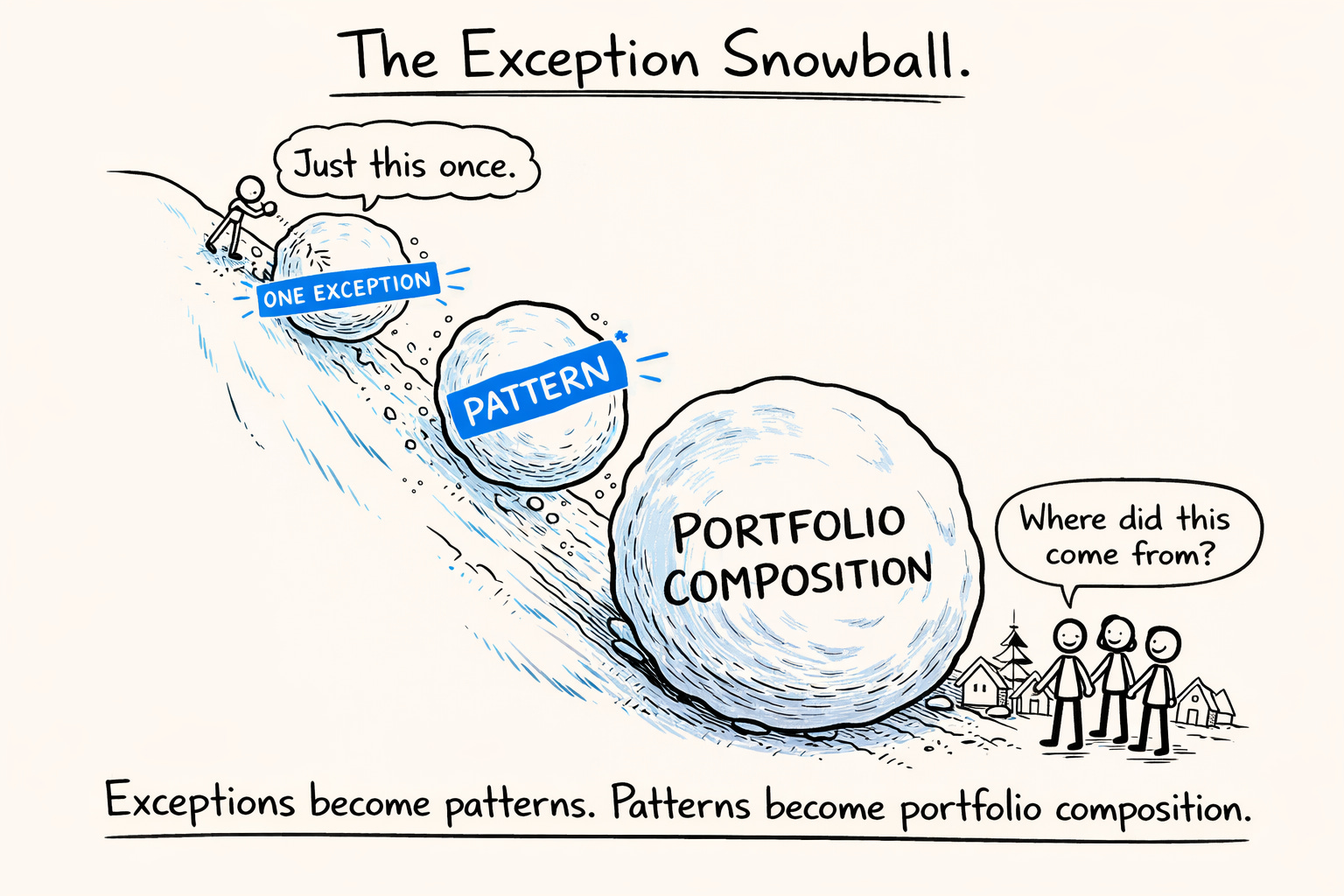

Quote-to-bind ratios shift in ways no one tracks at the product level. Risk selection drifts toward what’s easier to write, not what’s most profitable. Exceptions become patterns. Patterns become portfolio composition. The book that was intentionally curated becomes accidentally assembled.

The loss ratio delay makes this particularly insidious. Underwriting decisions made in Q1 don’t show up in loss experience until Q3 or Q4, sometimes later. By the time the numbers surface, the drift has been baked into the book for two or three quarters. Corrective action feels reactive rather than strategic, because it is reactive. The damage is already done; the question is how much more accumulates before the correction takes hold.

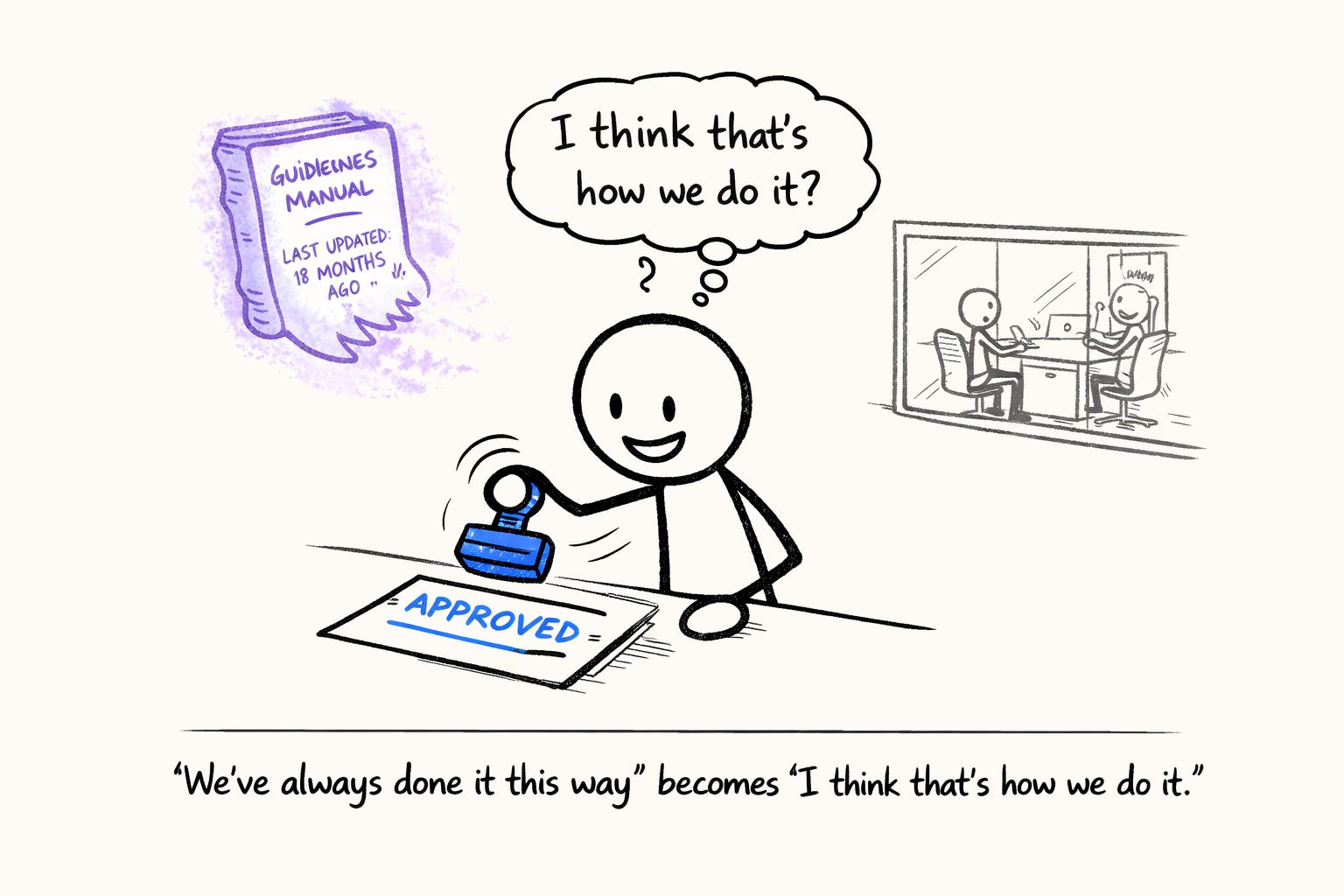

The cultural cost is harder to measure but equally real. The underwriting team feels stretched, not empowered. Institutional knowledge starts to degrade. “We’ve always done it this way” becomes “I think that’s how we do it.” The confidence that characterized the first product’s growth phase gives way to a persistent low-grade uncertainty.

Here’s the hard truth: underwriting discipline doesn’t fail because people stop caring. It fails because the system stops reinforcing the right behaviors. The second product doesn’t cause this. It reveals how fragile the discipline was to begin with.

The Human Cost of Diluted Discipline

The most painful consequence of the second product is not technical. It is human.

Underwriting attention is finite. The same senior underwriters who protect the first product’s discipline are now pulled into filings, edge cases, carrier conversations, and exception handling for the second. Time once spent refining appetite is now spent explaining variance.

Meanwhile, feedback loops degrade. Claims data arrives late and noisier. Attribution between products becomes less clean. Signals that once would have triggered corrective action are diluted by aggregation.

This is not bad underwriting. It is overextended underwriting.

Sometimes carriers feel the wobble before operators can prove it. Trust doesn’t vanish overnight, but it begins to wobble. Questions become more frequent. Reviews become more detailed. The relationship subtly shifts from partnership to oversight.

By the time leadership recognizes the dilution, reversing it requires more than effort. It requires structural repair.

Growth as Weight, Not Leverage

By this point, the pattern is clear. None of these failures are isolated. Together, they explain why growth feels heavier instead of easier.

The central mistake MGAs make when launching a second product is confusing growth with leverage.

Leverage simplifies. It standardizes. It compounds learning.

Weight accumulates. It introduces drag. It taxes cognition.

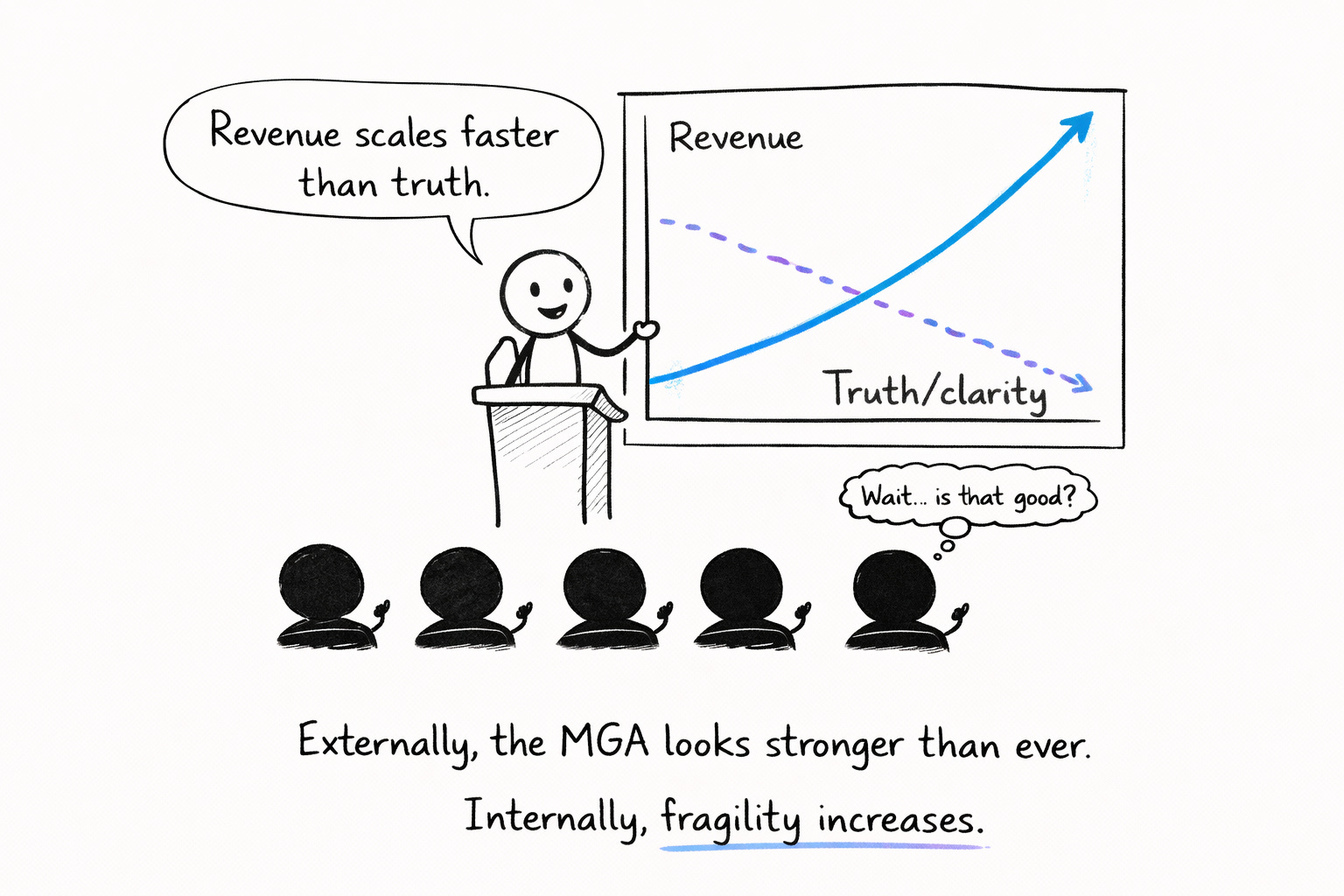

The second product adds revenue quickly, which masks its cost. Headcount grows, absorbing pressure without resolving it. Carriers remain supportive, because they want the product to succeed. Externally, the MGA looks stronger than ever.

Internally, fragility increases.

Audit preparation becomes stressful. Forecasting loses credibility. Strategic planning relies more on narrative than data. Leaders feel busy but less certain. Decisions are made faster, but with less clarity.

The organization is not collapsing.

It is carrying more than it was designed to hold.

The Compounding Effect

These three failure modes (schema drift, reporting fragmentation, underwriting discipline dilution) don’t operate in isolation. They reinforce each other in ways that accelerate the overall degradation.

Schema drift makes reporting harder, which increases fragmentation. Reporting fragmentation obscures the patterns that would reveal underwriting drift, so discipline problems go undetected longer. Discipline drift produces anomalies that eventually surface in carrier questions, and those questions reveal the schema and reporting gaps that enabled the drift in the first place. Each problem makes the others worse. Each problem makes the others harder to diagnose.

By the time leadership sees the full picture, the problems have been compounding for two to four quarters. The fix isn’t a single intervention. It’s a systemic rebuild that feels disproportionate to any single symptom. “We just need to clean up the data” becomes a six-month project. “We just need to tighten underwriting guidelines” requires rebuilding the feedback loops that atrophied. “We just need better reporting” means unwinding the workarounds that finance has come to depend on.

This is the emotional reality of the Second Product Syndrome: leadership didn’t miss anything. The signals were there, but they were distributed across teams, systems, and reports that don’t naturally talk to each other. No single dashboard captured the drift. No single meeting surfaced the fragmentation. The problems were visible in retrospect but invisible in real-time, because they accumulated in the spaces between functions rather than within them.

The second product didn’t cause the problem. It accelerated the exposure of problems that were already latent, waiting for enough operational complexity to reveal them.

The Operators Who Make It Work Anyway

Here’s what the previous sections don’t capture: most MGAs that launch a second product don’t fail. They struggle, they stretch, they accumulate technical debt and operational scar tissue, but they land on their feet.

This is not because the challenges are exaggerated. It’s because of the people.

The finance lead who rebuilds the reconciliation workbook for the third time because the carrier changed requirements again. The underwriting manager who stays late reviewing submissions that should have been referred but weren’t, quietly correcting course before the numbers go sideways. The ops analyst who notices the schema inconsistency six months before it would have surfaced in an audit, and fixes it without fanfare. The COO who absorbs the stress of competing priorities so the rest of the team can focus.

These are the people fixing the plane while flying it.

They don’t get the credit they deserve. The board sees revenue growth. The carrier sees bordereaux that (eventually) reconcile. Leadership sees a second product that launched on time. What they don’t see is the invisible load carried by operators who made it work through judgment, persistence, and an unreasonable number of late nights in spreadsheets.

The Second Product Syndrome is real. But so is the resilience of teams who refuse to let complexity win.

If you’re in the middle of this right now, stretched thin and wondering whether anyone notices: they should. And if they don’t, I do.

The second product is worth pursuing. Your team will figure it out. They already are.

When a Second Product Actually Works

There are MGAs that add a second product successfully. They’re rarer than they should be

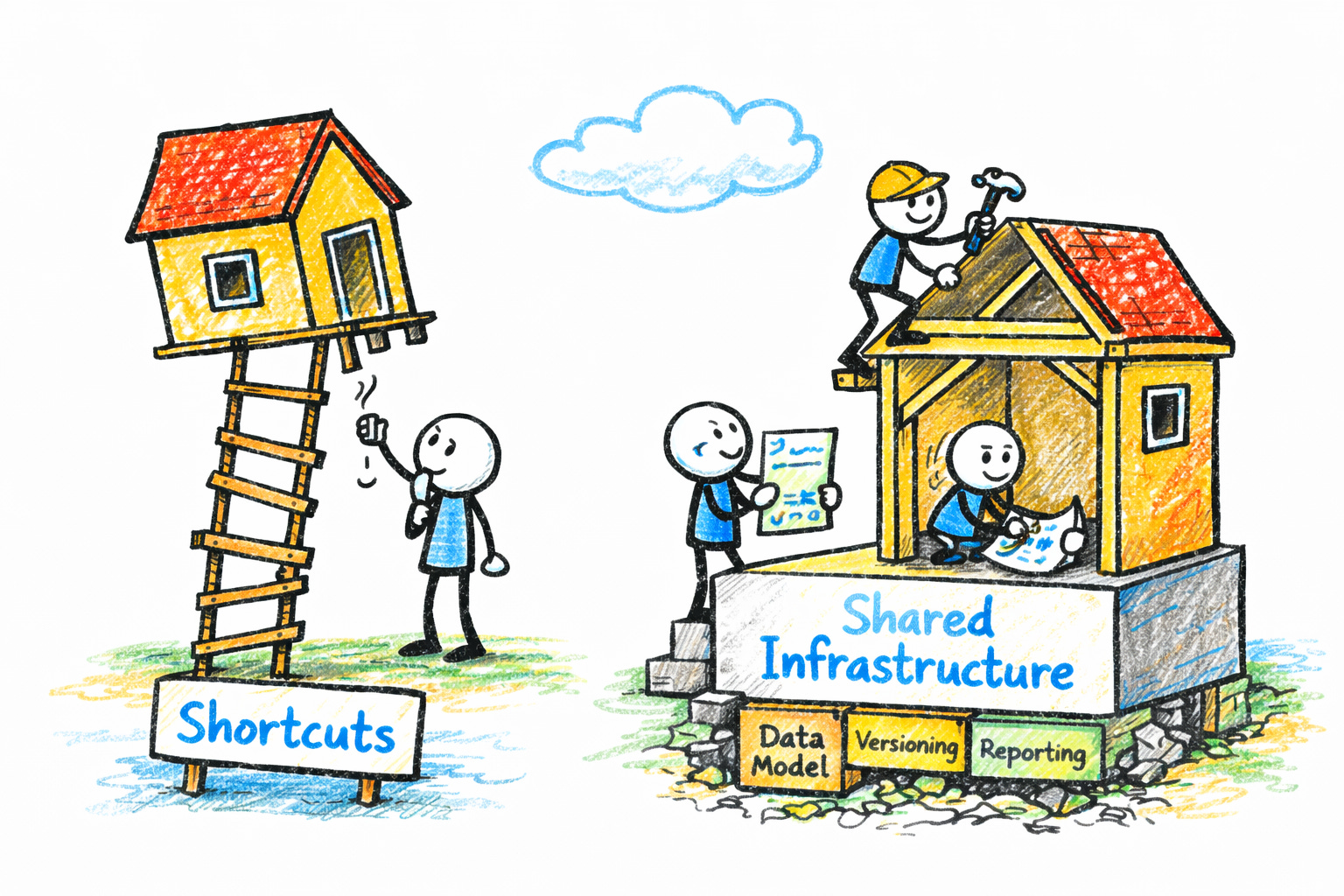

They treat the second product as a new company inside the company. Data schemas are designed explicitly, not extended casually. Reporting layers are unified before volume arrives. Underwriting ownership is clear and protected. Versioning is intentional. Reconciliation logic is documented.

Most importantly, they resist urgency.

They do not rush to market. They do not over-customize for early carriers. They do not ask operations to “figure it out later.” They build shared infrastructure, not shared shortcuts.

These MGAs understand that growth is optional, but repair is expensive.

The Operator’s Test

Before launching a second product, every MGA should be able to answer a few uncomfortable questions honestly.

Can you produce clean, inception-to-date reporting for your first product today, without caveats?

Can you explain every reconciliation rule in writing?

Can underwriting articulate where judgment ends and rules begin?

Can finance and underwriting agree on earned premium logic without qualifiers?

If not, the issue is not ambition.

It is readiness.

You are not blocked from growth.

You are not yet ready to carry more weight.

The Discipline of Saying Not Yet

The MGAs that endure are not the ones that grow fastest. They are the ones that understand their own structure deeply enough to respect its limits.

Restraint is not conservatism.

It is operational mastery.

In insurance, success does not reward speed. It rewards structural honesty. The discipline to say not yet, to reinforce foundations before adding load, is often the difference between a company that scales and one that slowly loses its grip on the truth.

Growth will come.

The question is whether you will still trust your systems when it does.

The MGAs that last know exactly how much weight they can carry, and refuse to pretend otherwise.

What This Means

The Second Product Syndrome isn’t a failure of ambition. It’s a structural consequence of growth.

The MGAs that navigate it well don’t do so by avoiding the second product. They do it by recognizing that the second product is a stress test, not of the team’s effort, but of the infrastructure’s maturity. They ask different questions before launch: not “can we sell this?” but “can our data model accommodate this without semantic drift?” Not “do we have underwriting expertise?” but “do we have the feedback loops to maintain discipline at split attention?” Not “can finance handle the reporting?” but “can finance handle the reporting without building another layer of reconciliation?”

These are harder questions. They don’t have obvious answers. They require looking at infrastructure not as a cost center but as a constraint on growth, one that either scales with the business or eventually limits it.

The question isn’t whether to grow. The question is whether your systems grow with you, or whether you discover their limits after the fact.

Much of my thinking here comes from building Faroe, a system designed specifically to survive these moments of expansion. It is a financial data model built to stay coherent as products multiply—version-controlled, inception-to-date, and auditable in how it explains every number. It turns bordereaux and premium movements into a reconciled view of what’s owed, what’s paid, and what’s disputed. What operators choose to do with that clarity—and with the time it returns—is up to them.

If you’re an insurance operator and this resonated, I hold office hours to help teams think clearly through the inflection points that come with scaling insurance programs.